In

In

Reserve Bank of India has been following a very conscious and comprehensive plan to boost digital payments in India. India’s payment strategy is driven by its three-yearly payment systems vision statements

Payment may seem to be one small component in the overall business and economic cycle. But in reality, payment is the moment of truth in any economic or commercial activity. Digital payments help an economy in many ways.

It makes the financial system far more efficient. By making the money move faster, it also enhances the efficiency of economy itself. It makes transactions transparent and easy to track—not just from the point of view of checking corruption but also from policy decision perspective. Finally, it makes access to essential services and products convenient for the common man, by removing artificial roadblocks that traditional transaction systems have created.

No wonder, an RBI-appointed High-Level Committee on ‘Deepening of Digital Payments’ headed by Nandan Nilekani—appointed in January 2019 to recommend ways and means of deepening digital payments and bridge any gaps that exist in the system—has in its report submitted in May 2019, recommended increasing per capita digital transactions by ten times in the next three years, by increasing the number of users of digital transactions by a factor of three, from approximately 100M to 300M in the corresponding period.

Digital Payment & Business

Payment is the culmination of a sales cycle. In a consumer business—where invoicing and payment are not too apart—payment is, in fact, business.

Hence, any business traversing the digital path today cannot ignore the criticality of digitalizing its payment options in order to make its transformation more effective. Digital payments help in achieving three critical objectives associated with transformation.

First and foremost, it transforms the customer experience. Payment is the last thing the customer (read consumer in a B2C business) is going to spend time about. By making it seamless, customer satisfaction is greatly enhanced. With the rise of electronic commerce—where digital payment is a pre-requisite (even if we erroneously call cash-on-delivery as e-commerce), the payment experience may make or break the business, especially where the payment is regular and periodic—like say bill payment.

Secondly, it greatly contributes to enhancement of efficiency of the business cycle. And finally, it greatly reduces the possibility of revenue leakage and hence results in a more effective revenue management.

With so much at stake, businesses—especially those helping them leverage technology—cannot take a mechanical approach to just ‘enable’ digital payments. Rather, they need to carefully plan their business—promotion, product customization and even warehouses—based on the digital payment trends.

This is what it means.

Say, in a village of 5000, ten people are interested in a video streaming services. With high speed data available, they can get that easily now. If you want to reach 1000 such villages, you are reaching 10,000 customers. But before digital payments came in, a provider had to either set up a costly collection mechanism or go through the mobile operators. Both being not-so-convenient an option for a smaller segment of target customers, the segment was ignored. With digital payment mechanisms, that neglected segment is a big opportunity now.

For consumer businesses to plan and promote well, they must even understand specific trends within payment. Tying up with card issuers may not give the desired results if people predominantly prefer mobile wallets. Similarly, trying to sell high value products through mobile wallet payments may not succeed. The fact that average value of transaction with a credit card is several times that of average value of transactions with a debit card has its own implications for planning sales—be it in finalizing rural/urban mix or tying up with card issuers.

Understanding of overall payments trends, how they are distributed among various instruments/mechanisms and how users of a particular mechanism behave while paying may provide crucial inputs to better business planning.

Apart from past data, the directions of payment regulations can give some visibility into how the payment trends may change over, say next 2 to 3 years.

The story essentially provides insights into such payment trends.

Indian Payment Trends, Circa 2019

That India—like the world at large—is moving towards digital transactions is not exactly news to anyone.

But only a deeper insight into the trends can give some realistic inputs valuable for business planning.

This includes data points, such as:

- The magnitude of overall growth

- Growth and share of various payment mechanisms

- The volume and value of transactions across each payment mechanism (which also gives average value of transaction)

- The pattern of growth over a period of time (we have taken five years)

Beyond pure data points, one needs to understand the veracity of perceptions and narratives in place. A wrong business decision based on a wrong assumption can be counter-productive.

Take, for example, the predominant narrative that demonetization kickstarted digital payment in India. In a decision which has been politically supported and opposed vigorously, only data can show the truth.

In an analysis in November 2017, one year after demonetization, we showed that demonetization, let alone initiating digital payment, had little impact on overall value of digital transactions, but it did significantly push up mobile wallet and debit card usage. In other words, demonetization did not impact depth of digital payments in India but significantly enhanced its breadth by expanding reach. We concluded that demonetization democratized digital payments—not a mean achievement in a country like India.

However, November 2017 was too early to gauge whether that impact was a lasting impact or an immediate disruption which was neutralized/regularized over a period of time. We will examine that now.

But it is not just demonetization’s impact. There are other common perceptions that actual data analysis may dispel. We will get into some of them here.

For the purpose of analysis, we have taken RBI data on only retail electronic payments. So, no RTGS (real time gross settlement) or no paper clearing systems have been taken into account.

The payment mechanisms that have been considered are EFT/NFT, IMPS, debit card (point of sales only), credit card (point of sales only), m-wallets and mobile banking.

RBI’s data for a five year period from financial year 2013-14 to financial year 2018-19 have been considered to better understand how the trends have evolved over the years.

Here are some of the insights payment data from RBI reveal—and what we could make out of them.

Overall growth in retail electronic payments over the five year period is 44% CAGR, supported by a strong, if not spectacular, growth of 39% in EFT/NFT which still accounts for 79% of the total retail electronic payments.

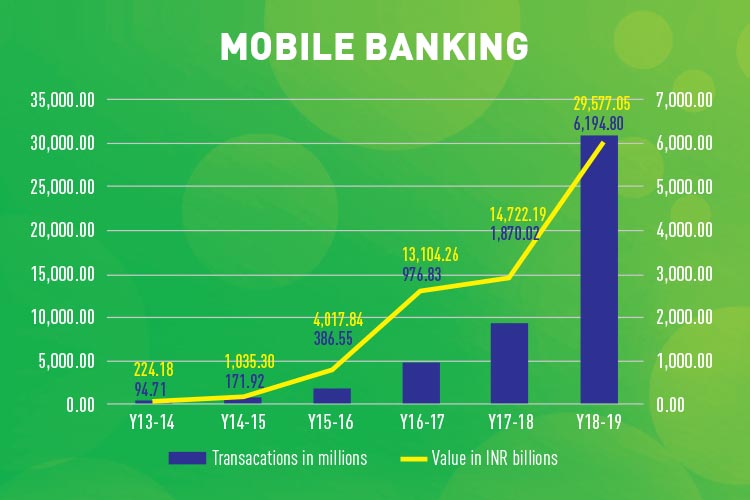

All the newer form of payment—IMPS, m-wallets and mobile banking—have grown by over 100% CAGR in this five year period. So, people essentially are shifting to newer forms.

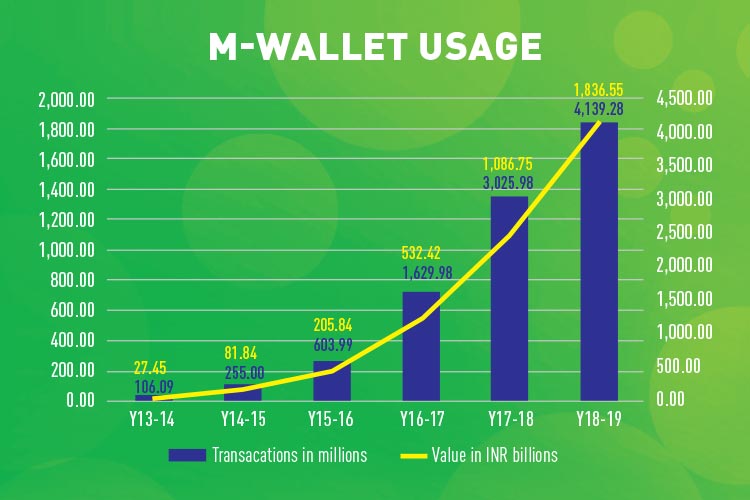

Mobile banking, which accounts for the second largest form of payment mechanism after EFT/NFT, has surprised everyone by growing 231% by volume and 101% by value in the single year 2018-19, on a much larger base than any of the other newer forms of payment. The buoyancy shown by m-wallets in 2016-17 on the wake of demonetization has cooled down in these two years. The segment, whose size of transactions is just about 6% of mobile banking, has grown by a modest (by Indian standard) 69%.

While it is understood that value of m-wallet transactions are smaller, what is surprising is that the number of transactions has shown an even lower growth—just 37%. The growth has steadily fallen from 170% in the demonetization year to 86% in 2017-18 and further halved to 37% in 2018-19.

So, what does this reveal? While no one can deny the role mobile wallets played in the two months after demonetization, it seems users have drifted away from mobile wallets, despite a number of mobile wallet players entering the business and some launching high profile marketing campaigns, supported by attractive promotional schemes like cashbacks.

While one section—having experienced electronic payment’s benefits—have moved to a more mature segment like mobile banking which uses their bank accounts and does not block money in wallets, another, which was forced to use mobile wallets because of cash problems using demonetization and its immediate aftermath, seems to have gone back to cash.

A regulator-imposed upper limit in m-wallets may have impacted the growth of total transaction value in mobile wallets. However, it cannot impact number of transactions too negatively if the user base is growing and users are actually using it.

This—of users shifting most definitely to a more mature service like mobile banking from mobile wallets—is one of the most revealing trends which has implications for how consumer businesses should plan for their digital businesses.

Cards may not be as new a payment mechanism as some of the other digital payment methods—and there may not be as disruptive trends to notice. But the usage data of cards show clear and specific trends that are meaningful for business decisions.

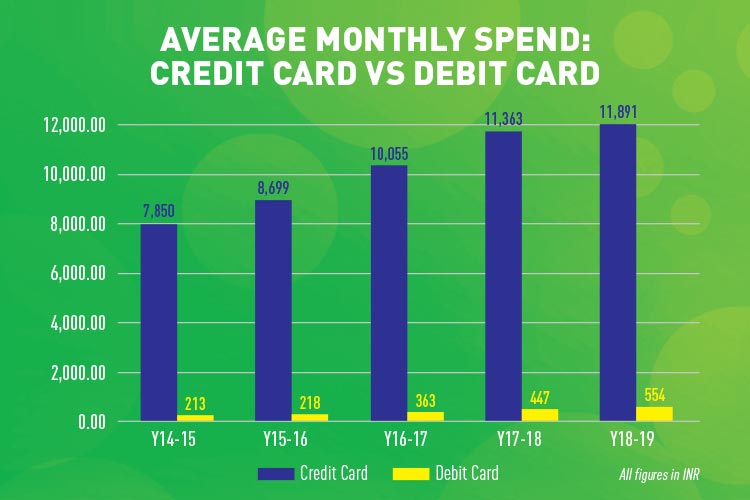

Credit cards debuted much before debit cards in India. Yet, it has been restricted to a niche segment—thanks partially to lack of a robust credit rating mechanism and the aversion to ‘credit’ as a cultural issue among Indians.

Today, in a country of one and half billion people, there are less than 50 million credit cards. With many users being multiple card holders, the actual number of people who use credit cards may not be more than 25-30 million.

Debit cards, on the other hand, have been ‘thrust’ upon the banking users. Today, every bank ATM card is a debit card that can be used to pay using a PoS terminal at a merchant location. Yet, most use it as simply to draw cash from ATMs.

The two card instruments—credit card and debit card—though hyphenated often are two different animals.

Look at the contrast. More than 924 million debit cards in circulation in India accounted for just INR 5935 billion worth of transactions on PoS (excluding cash withdrawal from ATMs). Just 47.1 million credit cards were used to spend more—INR 6033 billion to be precise—by its users.

A debit card user makes an average payment of INR 550 a month while a credit card user makes a payment of an average INR 11900 a month!

While growth of both has slowed down, debit cards got an impetus during demonetization. The instrument, which was showing an average growth of 30% before that, spent 108% more in the demonetization year 2016-17 as compared to the previous year, 20115-16. Credit cards did not witness any such spike.

With India’s new Payment Systems Vision 2021 clearly expressing an intent to move towards not just a less-cash society but also “to have a less-card India”, cards have a limited shelf life. Card companies have already started virtual cards and are beginning to market them aggressively.

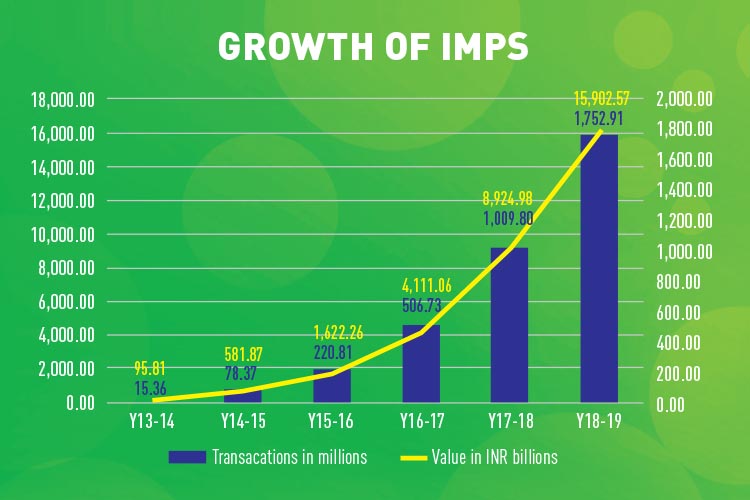

That brings us to IMPS—predominantly used for P2P transactions—which grew at a CAGR of 132% in terms of value in the five year period between 2013-14 to 2018-19 while showing a 108% CAGR in number of transactions in the said period. IMPS too accelerated during demonetization but not to the extent that mobile wallets and debit cards did.

Future Expectations

Contrary to popular perception, the surge in digital payments (even leaving out cards), did not start with either demonetization or Digital India. Reserve Bank of India has been following a very conscious and comprehensive plan to boost digital payments in India.

India’s payment strategy is driven by its three-yearly payment systems vision statements. It is interesting to examine how the vision has progressed. In 2005-08, the vision was “the establishment of safe, secure, sound and efficient payment and settlement systems for the country”. So, it was an intent, more than anything else.

The next vision document (2009-12) became bolder when RBI asserted that it wanted to “to ensure that all the payment and settlement systems operating in the country are safe, secure, sound, efficient, accessible and authorized”. It was now no more an intent; it was a mandate it gave to itself as a regulator by promising to the nation that it (RBI) would make it happen. Also, with the UPA government focused on aam aadmi and social inclusion, financial inclusion as an idea was taking strong roots among policy makers. That thrust saw RBI adding “accessible” to its Payment Vision. It was sort of a passive intent towards inclusion.

That passive intent became a proactive stance in the next vision document (2012-15) as it added the word “inclusive” to the vision. But that addition was along expected lines. What was more noteworthy were the addition of interoperability and compliance.

The vision statement for 2018—the first after a new government took over at the centre, maintained continuity. It did not add any such new deliverables captures the implementation thrust quite unequivocally, by identifying the four pillars of achieving the vision of less-cash society. Two of those pillars—responsive regulation and robust infrastructure—were mostly about detailing of earlier plans or some augmentation in terms of specific tasks. Customer centricity was a new thrust but the document was devoid of any ground-breaking new plans or ideas there. The real takeaway of the 2018 vision was effective supervision. It was a mechanism for making the players—banks and other payment operators—more accountable and also more responsible, without RBI explicitly acting like a school master to ensure that each task is achieved.

In the time-tested way of RBI policymaking, the new payment vision 2021, released in May 2019, took

the new idea introduced in Vision 2018—customer centricity—to make it the central focus of the new policy statement.

Vision 2021 concentrates on a two-pronged approach of, (a) exceptional customer experience; and (b) enabling an ecosystem which will result in this customer experience.

The Vision aims at:

a. enhancing the experience of customers

b. empowering payment system operators and service providers

c. enabling the ecosystem and infrastructure

d. putting in place a forward-looking regulation and

e. supported by a risk-focussed supervision

To achieve these goals, the Vision has four contours, it calls the 4 Cs–Competition, Cost, Convenience and Confidence. These four address innovative regulatory models like regulatory sandboxes for competition, efficiency through that competition helping reduce cost, better access to multiple payment systems and a no-compromise approach towards security that would enhance user confidence.

RBI has already completed a benchmarking exercise of India’s payment systems with 20 other countries, identifying each aspect (41 indicators in 21 areas) of India’s payment system as a leader (if ranked 1st to 3rd), strong (if ranked 4th to 9th), moderate (if ranked 10th to 15th) and weak (if ranked 16th to 21st).

According to that, India emerged as a leader across a dozen indicators. Those directly concerning with digital payment are:

- Regulation of costs of payment systems

- Number of debit cards issued

- Availability of alternate payment systems

- Share of e-money in the payment systems

- Citizen to government payment

- Business to government payment

- Government to business payment

India’s payment system was found to be lacking (weak) in the following digital payment areas which RBI will address:

- Rate in decline of cheques

- Check volume payment

- Share of card payments in payment system

- People per PoS

- Value of debit card and credit card payments to cash

- in circulation

- Volume and growth of direct debits

- Share of direct debit in payment system

- Digital payment of utility bills

- Public Mass Transportation payment

While some of them such as cheque volume and decline of cheques cannot be addressed overnight, digital payment of utility bills can be significantly enhanced with right capacity building and policies.

In January, RBI had appointed a High-Level Committee on ‘Deepening of Digital Payments’ headed by Nandan Nilekani. The committee has already submitted its report in May. It has recommended a number of steps to RBI, government and businesses.

Some of the important recommendations include:

- Growing digital transactions volume by a factor of 10 in three years

- Better defining digital payment and strengthening data collection and tracking

- Addressing the issues of interchange fees and other issues in regular intervals

- Including non-banking entities in payment ecosystem

- Setting up of an Acceptance Development Fund to be used for improving acquiring infrastructure at Tier IV, V and VI areas, with contribution from card issuers and RBI

- Each merchant should support at least one digital mode viz BharatQR, BHIM UPI QR, or cards

- Allowing customers to initiate and accept a reasonable number of digital payment transactions with no charges

- Creating online dispute settlement systems by all payment operators including NPCI

- Continuous monitoring and improvement of transaction failures

- Operationalization of a FIN-CERT for oversight, and monitoring security of the digital payment systems

- Creation of a central fraud registry, that tracks all reported fraud

- Regular surveys to address digital payment issues and perceptions

- Promotion of digital transactions at rural farmer markets

- Promotion of interoperable standards for transit payments

In addition to these key recommendations, the committee has suggested capacity building, promoting digital literacy, tracking inclusion, enhance accessibility, use vernacular languages and similar initiatives to promote digital payments.

Businesses should expect some of these recommendations to become realities in next two-three years. It is advisable that they actively follow the real rollout on ground to get a realistic assessment of where digital payment is going. That will help them prepare better for the new real digital India, where the culmination of business—payment—is fully digital.

Real digital transformation strategies cannot ignore this most fundamental environmental change.

Comments

India Generic Viagra Order

India Generic Viagra Order https://buyciallisonline.com/ - Buy Cialis difference entre cialis et generique <a href=https://buyciallisonline.com/#>Cialis</a> How To Use Propecia

India Generic Viagra Order

India Generic Viagra Order https://buyciallisonline.com/ - Buy Cialis difference entre cialis et generique <a href=https://buyciallisonline.com/#>Cialis</a> How To Use Propecia

Add new comment