In

In

The worldwide public cloud services market, including Infrastructure as a Service (IaaS), System Infrastructure Software as a Service (SISaaS), Platform as a Service (PaaS), and Software as a Service (SaaS), grew 24.1% year over year in 2020 with revenues totaling USD 312 billion, according to IDC’s Worldwide Semiannual Public Cloud Services Tracker.

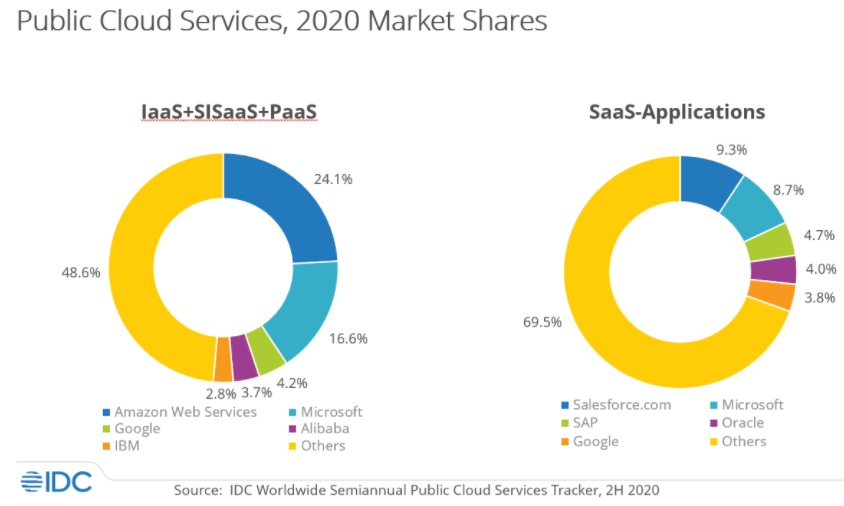

Spending continued to consolidate in 2020 with the combined revenue of the top 5 public cloud service providers (Amazon Web Services, Microsoft, Salesforce.com, Google, and Oracle) capturing 38% of the worldwide total and growing 32% year over year. Thanks to an expanding portfolio of SaaS and SISaaS offerings, Microsoft now shares the top position with Amazon Web Services in the whole public cloud services market with both companies holding 12.8% revenue share for the year.

"Access to shared infrastructure, data, and application resources in public clouds played a critical role in helping organizations and individuals navigate the disruptions of the past year," said Rick Villars, group vice president, Worldwide Research at IDC. "In the coming years, enterprises' ability to govern a growing portfolio of cloud services will be the foundation for introducing greater automation into business and IT processes while also becoming more digitally resilient."

While the overall public cloud services market grew 24.1% in 2020, consistent with the past four years, the IaaS and PaaS segments have consistently grown at much faster rates. This highlights the increasing reliance of enterprises on a cloud foundation built on cloud infrastructure, software defined data, compute and governance solutions as a Service, and cloud-native platforms for application deployment for enterprise IT internal applications. IDC expects spending on foundational cloud services (especially IaaS and PaaS) to continue growing at a higher rate than the overall cloud market as resilience, flexibility, and agility guide IT platform decisions.

"Cloud service providers are rapidly expanding their portfolio of infrastructure and platform services to address confidential computing, performance intensive computing, and hybrid deployment scenarios," said Dave McCarthy, vice president, Cloud and Edge Infrastructure Services. "Extending these foundational cloud services to customer premises and communications networks enables a broader set of use cases than previously possible."

"The high pace of growth in PaaS, IaaS, and SISaaS, which combined account for about half of the public cloud services market, reflects the demand for solutions that accelerate and automate the development and delivery of modern applications" said Lara Greden, research director, Platform as a Service. "As organizations adopt DevOps approaches and align according to value streams, we are seeing PaaS, IaaS, and SISaaS solutions become increasingly adopted and, at the same time, grow in the range of services and thus value they provide. Innovations in edge and IoT use cases are also contributing to the faster rates of growth in these markets."

"SaaS applications is the largest and most mature segment of public cloud with 2020 revenues of USD 148 billion. Organizations across industries hastened the replacement of legacy business applications with a new breed of SaaS applications that is data-driven, intuitive, composable, and ideally suited for more distributed cloud architectures. Organizations looking for industry-specific applications can choose from a growing assortment of vertical applications. The SaaS apps market is dominated by a longtail of providers that account for 65% of the total market," said Frank Della Rosa, research director, SaaS and Cloud Software.

|

Worldwide Public Cloud Services Revenue and Year-over-Year Growth, Calendar Year 2020 (revenues in USD billions) |

|||||

|

Segment |

2020 Revenue |

Market Share |

2019 Revenue |

Market Share |

Year-over-Year Growth |

|

IaaS |

USD 67.2 |

21.5% |

USD 50.2 |

19.9% |

33.9% |

|

SaaS – System Infrastructure Software |

USD 49.2 |

15.7% |

USD 40.2 |

16.0% |

22.4% |

|

PaaS |

USD 47.6 |

15.2% |

USD 36.1 |

14.4% |

31.8% |

|

SaaS – Applications |

USD 148.4 |

47.5% |

USD 125.2 |

49.7% |

18.6% |

|

Total |

USD 312.4 |

100% |

USD 251.7 |

100% |

24.1% |

|

Source: IDC Worldwide Semiannual Public Cloud Services Tracker, 2H20 |

|||||

Looking at the segment results, a combined view of IaaS, SISaaS, and PaaS spending is relevant because it represents the foundational set of services that end customers and SaaS companies consume when running, modernizing, building, and governing applications on shared public clouds. In the combined IaaS, SISaaS and PaaS market, the top 5 companies (Amazon Web Services, Microsoft, Google, Alibaba, and IBM) captured over 51% of global revenues. But there continues to be a healthy long tail, representing nearly half the market total. These are companies with targeted use case-specific PaaS services or cross-cloud compute, data, or network governance services. The long tail is even more pronounced in SaaS, where customers growing focus on specific outcomes ensures that over two thirds of the spending is captured outside the top 5.

|

Worldwide Public Cloud Services Revenue and Year-over-Year Growth, Calendar Year 2020 (revenues in US$ billions) |

|||||

|

Segment |

2020 Revenue |

Market Share |

2019 Revenue |

Market Share |

Year-over-Year Growth |

|

IaaS |

$67.2 |

21.5% |

$50.2 |

19.9% |

33.9% |

|

SaaS – System Infrastructure Software |

$49.2 |

15.7% |

$40.2 |

16.0% |

22.4% |

|

PaaS |

$47.6 |

15.2% |

$36.1 |

14.4% |

31.8% |

|

SaaS – Applications |

$148.4 |

47.5% |

$125.2 |

49.7% |

18.6% |

|

Total |

$312.4 |

100% |

$251.7 |

100% |

24.1% |

|

Source: IDC Worldwide Semiannual Public Cloud Services Tracker, 2H20 |

|||||

Add new comment